LIFE INSURANCE

Protect Your Future,

Protect Your Loved Ones.

From affordable term life to advanced Indexed Universal Life (IUL) with Long-Term Care benefits ;

Personalized coverage for families, individuals, and those planning for the future.

Life Insurance is not One-Size-Fits All

and Neither is Our Guidance

- The right policy for a 30-year-old with a young family is completely different from the right policy for someone building retirement wealth — or a senior who wants final expenses covered without burdening their children.

- Our bilingual team evaluates your specific situation: your income, debts, family needs, and long-term goals. We compare policy types, explain the trade-offs clearly, and recommend coverage that actually fits — not the most expensive option.

- Whether you’re buying your first policy, upgrading existing coverage, or exploring IUL as a wealth-building tool, we guide you through every step.

Protecting your family is one of the most important financial decisions you’ll make. We focus on preparing ahead — evaluating your options early, so your loved ones are financially secure no matter what happens.

MBA. Quyen Le

Professional of Financial

and Professional Viet Nam Consular

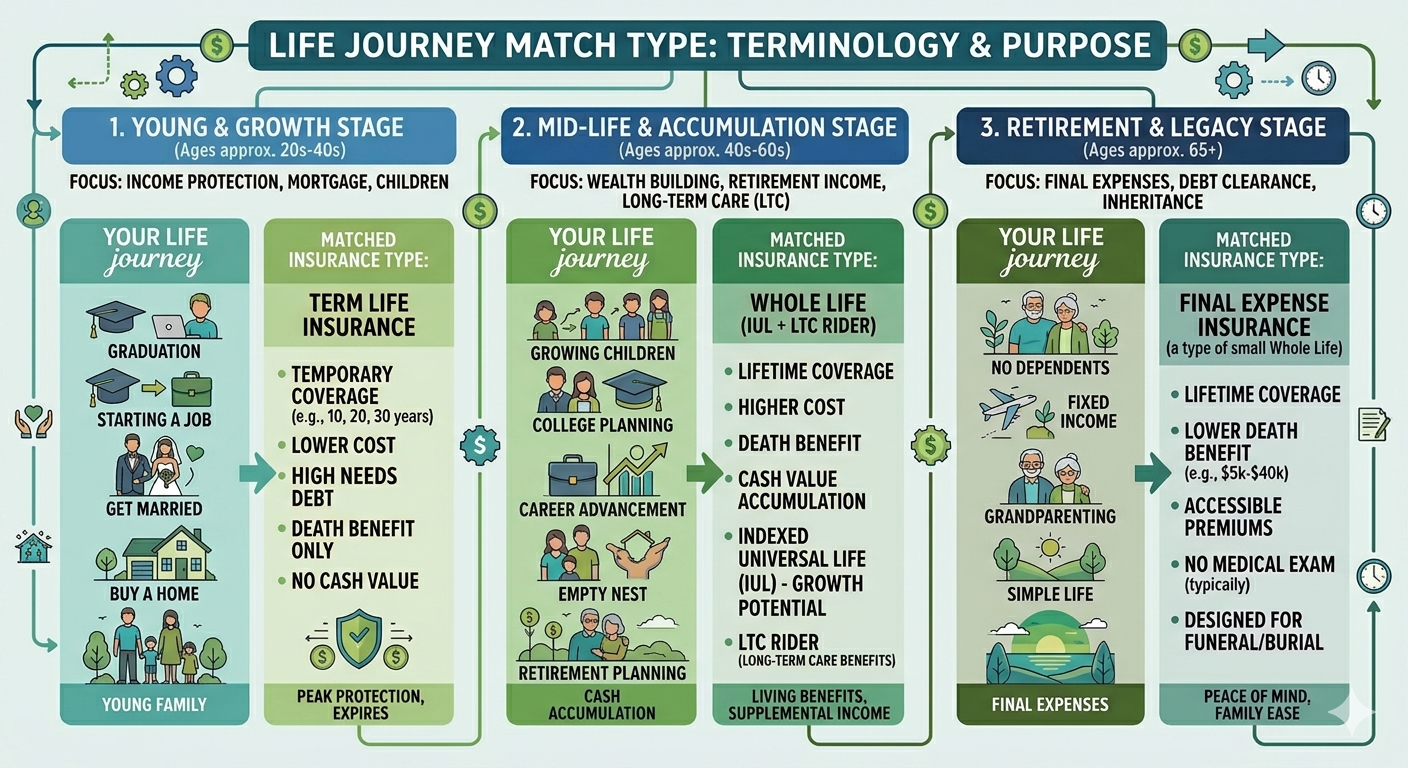

What stage of life are you planning for ?

Select your situation to see the coverage that fits you.

Plan Details & Coverage Guides

Expand each plan type for key details, best-fit profiles, and what to expect. All content is educational

we’ll tailor everything to your specific situation during your free consultation.

Term Life & Whole Life Insurance

TERM LIFE INSURANCE

- Coverage for a specific term: 10, 20, or 30 years

- Death benefit paid only if you pass during the term

- Most affordable type of life insurance

- Best for: young families, mortgages, loans, temporary income replacement

- Living Benefit Rider available — access death benefit early if diagnosed with critical, chronic, or terminal illness

WHOLE LIFE INSURANCE

- Lifetime coverage — never expires as long as premiums are paid

- Builds a cash value savings component over time

- Higher premiums than term, but permanent and predictable

- Best for: long-term financial planning, estate planning, leaving a legacy

- Cash value can be borrowed against for emergencies or retirement

How to choose: If budget is the priority right now → start with Term. If you want coverage that never expires and builds value → Whole Life. We’ll run the numbers for both and show you the comparison.

Indexed Universal Life (IUL) + Long-Term Care Rider

How Indexed Universal Life (IUL) Works

CORE IUL FEATURES

- Death Benefit: Guaranteed payout to beneficiaries

- Cash Value Growth: Accumulates tax-deferred, linked to a stock market index (e.g., S&P 500) — but your money is not directly in the market

- Downside Protection: A floor (usually 0–1%) means you never lose cash value due to market drops

- Flexible Premiums: Adjust payment amounts and timing as your income changes

TAX ADVANTAGES

- Cash value grows tax-deferred — no annual tax on growth

- Policy loans can be tax-free if structured correctly

- LTC benefit withdrawals are typically tax-free

- Death benefit passes to beneficiaries income-tax-free

- Note: Returns are capped at a maximum credit rate. Fees and cost of insurance reduce cash value growth. Requires long-term commitment.

Adding the Long-Term Care (LTC) Rider — How It Works

STEP 1 You Pay Premiums

- Premium payments fund your permanent IUL policy and build cash value over time

STEP 2 LTC Need Arises

- If you can no longer perform 2 of 6 daily living activities (ADLs) or have cognitive impairment, the rider activates

STEP 3 Benefits Pay Out

- You access part of your death benefit early — tax-free — to cover nursing home, assisted living, or in-home care costs

IF LTC NOT USED Beneficiaries Receive Full Death Benefit

- Any unused LTC benefit remains as a guaranteed death benefit — nothing is lost

Who it’s best for: Those who want permanent life insurance · People concerned about LTC costs but don’t want a separate standalone policy · Those seeking tax-advantaged savings with flexibility. Nursing home / assisted living costs: $100,000– $200,000+ per year — and Medicare does NOT cover long-term care.

Universal Life Insurance (UL)

KEY FEATURES

- Flexible premiums — adjust payments as your financial situation changes

- Adjustable death benefit — increase or decrease coverage over time

- Cash value growth tied to interest rates or index performance

- Permanent coverage — does not expire like term insurance

BEST FOR

- People who want flexibility in how much they pay year to year

- Those who want some investment growth without the full commitment of IUL

- Clients whose income fluctuates seasonally or by business cycle

- Those who want permanent coverage but need more payment flexibility than Whole Life allows

Final Expense Insurance

HOW IT WORKS

- Coverage amount: typically $5,000–$50,000

- Simplified underwriting — no medical exam required in most cases

- Guaranteed acceptance options available for qualifying ages

- Higher cost per dollar of coverage compared to term or whole life

- Pays out directly to beneficiaries — they use it as needed

BEST FOR

- Seniors who want to cover funeral and burial costs

- Those with small outstanding debts or medical bills

- Individuals who may not qualify for larger policies due to health

- Families who want to avoid financial burden during bereavement

- Anyone who wants to lock in coverage quickly with minimal paperwork

Planning tip: Average U.S. funeral costs range from $8,000–$12,000. Final Expense Insurance ensures your family won’t need to fundraise or go into debt to honor your wishes.

* Insurance policies and coverage options vary by carrier, state, and individual qualification. All content for illustrative purposes only.

Frequently Asked Questions

Term life provides affordable coverage for a fixed period (10, 20, or 30 years) — ideal for mortgages, young families, and temporary income replacement. Whole life provides coverage for life with a cash value component that grows over time. Term is cheaper upfront; whole life builds long-term value. We'll compare both side by side for your situation.

IUL policies combine life insurance with a cash value account linked to a stock market index (like the S&P 500). When the index performs well, your cash value grows — but you're protected from losses by a guaranteed floor (typically 0–1%). This means market upside without market risk on your principal. Cash value grows tax-deferred and policy loans can be taken tax-free if structured properly.

An IUL with an LTC rider gives you two protections in one policy — a death benefit for your beneficiaries and access to funds if you ever need nursing home, assisted living, or in-home care. It's ideal for those who want permanent life insurance and want to avoid a separate standalone LTC policy. If LTC is never needed, the full death benefit goes to your beneficiaries — nothing is lost.

A general starting point is 10–12 times your annual income, but your real needs depend on your mortgage balance, number of dependents, outstanding debts, future education expenses, and your spouse's income. We conduct a full needs analysis before recommending any coverage amount — so you're not over-insured or under-protected.

Average U.S. funeral costs run $8,000–$12,000 and continue to rise. Pre-planning with a Final Expense policy locks in today's prices, relieves your family of financial and logistical burden during a difficult time, and ensures your personal and cultural wishes are honored. It also avoids the need for family members to fundraise or go into debt at the time of loss.

Ready to secure your family's future

with the right life insurance ?

Start Planning Your Life Insurance

Fill out the form below and our team will contact you within 24 hours to discuss your life insurance needs.